With the debt ceiling coming up, stories of debt alarmism are shooting around like crazy. We’re back to seeing the ever-growing debt clock, along with fears of hyperinflation and questions of when foreigners will stop funding the US government by purchasing its debt. The famous Stanley Druckenmiller had a big speech arguing about how the US government needed to address its spending problem now by cutting 40% from its budget including almost all of our “entitlement” spending like Social Security.

One question that these debt alarmists always fail to ask is why foreigners are buying US debt. This seems odd, like blaming the entire 2008 global financial crisis on greedy subprime borrowers without ever asking who was lending so much on mortgages and why. The truth is, capital seeking a home will always find one. Take a look at China … they throw out their GDP targets, which are then achieved by local governments borrowing whatever it takes to get them there. They’ll invest in bullet trains, subway stations, property developments (even empty ones), property development companies – they’ll always find something.

Back to US debt – why are so many foreign entities buying it? Where are they getting the money?

This brings us to a critical issue that debt alarmists never seem to talk about – the trade deficit:

It’s amazing when you bring a historical perspective to our alarming debt problems. Debt to GDP was low during the period of sustained inflation, and recently CPI inflation problems were transitory, from the oil supply shocks of 2008 to the enormous shocks from the total economic disruptions of 2020-2021. If CPI inflation is driven primarily by debt today, then why wasn’t it a problem while Debt to GPD soared from 2009 thru 2012? The simple answer is that there are other factors at play.

Isn’t this debt growth unsustainable? Foreigners can’t buy our debt forever, can they?

If foreigners are getting the money to buy US assets from their trade surplus, then they can keep buying US debt and other assets as long as the trade surplus persists. In fact, they have to in order to keep it. Massive trade deficits mean that the US is supplying foreigners with massive amounts of US dollars – because Americans pay for goods in US dollars. If the rest of the world decides to convert these dollars into other currencies, then those currencies will rise in value relative to the dollar and the goods from those countries will be more expensive to US consumers.

Imagine you have a foreign government like China that decides it doesn’t want to accumulate any more US assets, but still wants to remain export competitive. Then one of two scenarios happens – either the Chinese currency begins to rise and the Chinese government intervenes to keep its exports competitive, or the Chinese government gives more support to state-operated-vehicles which produce exports and uses the dollars to accumulate Gold, Belt-and-road country debt, or other foreign assets. Those dollars are still accumulated by exports to the US, and they still can only come back by foreigners purchasing US assets such as debt, and the value of this US debt.

In short, foreign countries are fostering a permanent trade surplus with the US. As long as this persists, they will accumulate dollars which must be spent to purchase US assets. So why do they do it?

The US system has open capital markets with strong legal protections for foreign investors. Foreign countries that focus on supporting “export competitiveness” often have closed capital markets or more dubious legal structures. The leaders of powerful exporting firms are often very rich, quite happy to accumulate personal wealth in large Western countries, and they want to keep the status quo. At the same time, any disruption to their exporting machines leads to massive layoffs and protests from workers who live just above the subsistence level. It is extremely difficult for foreign export-oriented countries to change this system, so they keep exporting to the US and they keep buying US debt and other assets.

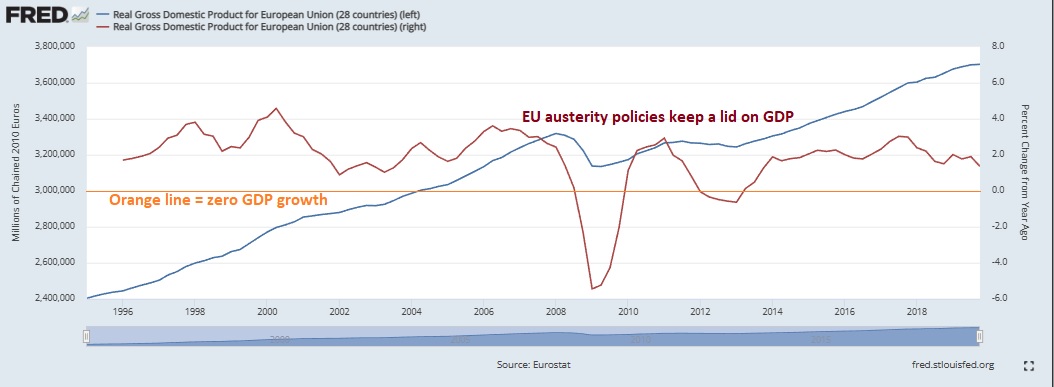

What happens if the US government decides to fight the deficit through spending cuts? The European Union actually did this during the early 2010’s. Here are some charts:

US GDP Growth for comparison:

Note that as the EU moved to a trade surplus from 2012 through 2019, and that trade surplus had to go somewhere. During that time, US GDP continued to grow as the US trade deficit remained large – so the US was able to help absorb the trade surplus of the EU as the system rebalanced.

If the US successfully cut its deficit, it would also crush the trade deficit by crushing domestic demand. However, the necessary GDP drop could be much lower as many foreign countries have policies in place which react to support their trade surpluses – policies which would lead to a soaring US dollar to help offset the drop in US demand with regard to their exports. Ultimately the system would have to find a new balance, which would involve a combination of rising US corporate and/or consumer debt, lower US demand, and higher unemployment in the US and even more in the large foreign exporters to the US.

So what should we do?

In my opinion, US government debt gets far too much focus and we should think about what our real goals are. Take a look at a chart of countries with debt-to-gdp ratios like this one:

https://www.worldeconomics.com/Debt/

When you look through these charts, you’ll notice right away that most of the popular destinations for people to want to move are on the left side, though not exclusively. There is a bit of a range here. The point is that Debt to GDP is not the most important thing to look for in a country, that many other factors are much more important such as high standards of living, personal freedoms, rule of law, and so on.

Perhaps we should consider these factors before plunging the country and the world into depression while cutting our social safety nets at a time of peak wealth inequality in a Quixotic charge against the Giant of US Government Debt.

Closing thoughts on markets

As for markets this week, they’re still in a painstakingly slow consolidation around 4100 in the S&P 500. Regional banks are still under stress as Jamie Dimon voices threats of banning short selling on banks and investigating anyone who would dare short a bank stock. No banks are fell to the FDIC this week, and breadth measures continue to diminish as Apple became more valuable than all the companies in the Russell 2000 combined.

I didn’t make any trades this week and the markets barely moved, so I’m not going to update my holdings today. One interesting thought though – stock market consolidation is a lot like tug-of-war: very little movement followed by a large move when the bullish or bearish forces collapse.