It’s been a crazy couple of weeks for precious metals.

The weekly candles on the top chart still show a decent uptrend case, with gold breaking out and successfully backtesting a bull flag formation, and carving out a potential reverse head-and-shoulders pattern. Gold slipped below the 50 week moving average but is well above the 200 week.

The daily candles on the bottom chart are not that clear. You have a descending channel with a false breakout in January forming a bearish double-top and hitting a new low in March, where it formed a bullish double-bottom, broke out of the descending wedge, but failed to re-test the 1950 double top and landed above support around 1750. The 50 day moving average plummeted below the 200 day back in February, which is bearish, and just recently re-tested that level. However, the price remains below and the 200 day moving average topped and started trending downward. This spells trouble unless gold can break to the upside fairly soon.

The lines you draw on technical analysis are more art than science and really only give you an indication of trend. These trend lines are important in determining whether the big money is moving into or out of the asset class. Imagine yourself running a large fund, where you need to buy or sell a lot to move your performance needle, and that amount will move the market. If you are selling out, then you are slowly selling rallies but trying not to make the price plummet. If you are accumulating a position, then you are slowly buying dips but trying not to make the price rocket in the short term.

Speaking of what the big players are doing, here’s a chart from cotpricecharts.com (choosing basic charts, then GC):

On the chart above, large speculators have trimmed down their long positions considerably while commercial has reduced its short positions considerably. I put in the orange lines and text so that you could see how these levels reacted at significant points in the gold price chart.

The commercials here are gold miners. They spend large sums developing mines and conducting mining operations, and these short positions allow them to hedge so that they won’t go under if the gold price collapses. There is a considerable time lag between getting the metal out of the ground, refined, and sold to market so they use these positions to lock in a profitable price for this work. When they can buy back their contracts for the same price as mining new metal, then they will start closing out these contracts and their short position shrinks. The other side is large and small speculators who are simply betting that the price of gold goes higher. In many ways it just mirrors the gold miner positions, but you could also interpret it as some of the speculative longs being washed out and as investor sentiment becomes more bearish.

Essentially, commercial short positions tend to be a lot smaller at lows and a lot bigger at highs (inverse for large speculators). I remember seeing charts like this with very rare neutral positions in commercials back in 2018-2019 before price spikes. Take this all with a bit of a grain of salt though, because the movement of commercial positions is not so much predictive as by design. If gold producers can buy gold cheaper on the Comex then it can mine, it will start closing its comex positions and then start shuttering mines. Supply goes down and eventually price goes back up. This activity is even more apparent in the Uranium sector, where you had big producers like Cameco, who shut down their big Cigar Lake mine around 2019-2020 and then purchased cheap Uranium on the spot market to fill their sales contracts.

I’ll finish this segment with why I’m positioned so heavily in precious metals miners.

- Precious metals topped in 2011 and then carved out a bottom over the next decade. During that time, their was a lot of consolidation in the sector along with a lot less exploration and mine development. Exploration and mine development take years to build out, so supply will take time to increase and overtake demand.

- There tends to be a powerful sector rotation in the markets that changes every decade. Since 1990 you had alternating bull/bear runs of tech then commodities, and it makes sense to me that the current major tech run will turn in favor of commodities at some point.

- Gold remains an important asset in the global financial system and central banks are still net buyers. Many countries do not like being overly dependent on the US dollar after our overuse of weaponized sanctions, and gold is one of the assets that countries will turn to in order to diversify from their US dollar holdings.

- I am very worried about the leverage in our financial system. A small amount of selling can avalanche with margin calls into a market rout.

- The heavy “downside bets” positions in my portfolio, containing index puts and TLT calls, reflect this fear. If this happens, I expect precious metals to get hit with everything else, but to a lesser extent and with a quicker recovery just like in 2009.

- The market could avoid a significant correction for years and my “downside bets” positions – which are all long-dated options – can get crushed. If this happens, then my positions in mining stocks should be okay because they are primarily shares so they have no expiration date. These miners are making really good money at current precious metals prices, and they won’t collapse to zero even if current market trends prevail for 2 more years.

- The market is rising along with heavy liquidity. If the nearly $1 billion in reverse-repo action combined with continuously expanding mortgage and margin debt reflects a financial system that is flooded with money looking for any opportunity to grow, then sector rotation is very natural and precious metals miners will look like bargains at some point.

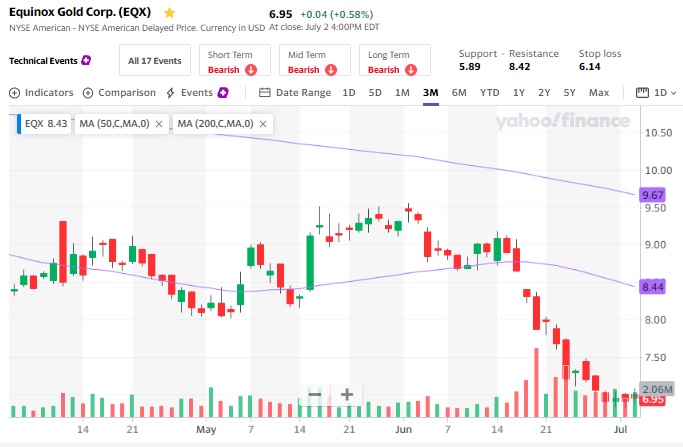

That being said, I can’t help but share this chart:

Equinox Gold is one of my bigger precious metals plays. I’ve been following it for a couple years because director Ross Beaty has a long successful history in the sector. My portfolio got hit pretty hard with the recent share price collapse from $9.50 down below $7.00. I tried really hard not to add much to this apparent falling knife, but I did break down and add some. This last two weeks has been really hard on a lot of the miners though, so I’ve been focusing on adding to ones that I’ve been meaning to increase my stake in.

Here’s where my portfolio ended up:

- DOWNSIDE BETS (38.2%)

- 28.0% TLT Calls

- 5.2% IWM Puts

- 3.5% QQQ Puts

- 1.5% EEM Puts

- PRECIOUS METALS (45.2%)

- 10.4% AG (Silver), mainly shares some calls

- 9.2% SAND (Gold, Silver & others), all calls

- 5.4% EQX (Gold), shares & calls

- 4.9% SILV (Silver)

- 4.4% MTA (Gold & Silver)

- 3.4% SILVRF (Silver)

- 3.0% LGDTF (Gold)

- 1.6% NEM (Gold, Copper & Silver), all calls

- 1.6% RSNVF (Silver)

- 0.7% SSVFF (Silver)

- 0.7% GOLD (Gold, Copper), all calls

- OTHER COMMODITIES (8.7%)

- 4.9% NOVRF (Nickel/Copper)

- 1.9% UUUU (Uranium, Vanadium, Copper)

- 1.2% CCJ (Uranium)

- 0.8% BQSSF (Uranium)

- CANNABIS (6.2%) split btw CRLBF, GTBIF & TRSSF

- CRYPTO (3.5%) all ADA

- CASH (-1.8%)

I changed my previous gold/silver breakdown into an overall precious metals category because a lot of the mining and royalty streaming companies have some of both. I also put in a rudimentary description of what their main exposures are.

My cash position is slightly negative because I dipped into margin a bit. Having a margin account allows me to buy into dips when they occur, but I typically like to keep this slightly positive.

TLT was strong this week and my account actually managed a 2.9% gain (vs a 10.8% loss last week). I calculate this ex-crypto (because it is in a different account) and I subtract out deposits so that I can see actual portfolio gains and losses. I did sell a couple of TLT contracts off this week to move that toward miners, but I didn’t sell as many as planned because my limit sell orders didn’t hit. Although I expect long treasury rates to continue lower, I’m not sure we’ll revisit last year’s low so I don’t mind repositioning some of that to buy into miners on weakness.

I suppose I’ll end be re-stating my nuanced position on inflation. I believe that we are in a debt-driven asset bubble, and that costs of living have been skyrocketing this last decade – primarily in housing which has become a speculative investment asset – while wages have remained subdued. Overall deflationary forces of high debt greatly eclipse our fiscal deficit spending, and many of the inflationary forces we’ve been seeing are transitory. However, inflation/deflation is very nuanced and some commodities are set to do really well based on supply/demand constraints.

- The excess supply available in oil will keep it’s price somewhat capped, though I don’t expect it to collapse down to last year’s levels unless we hit a major deleveraging event.

- Lumber spikes were transitory – it grows on trees and there is no shortage of supply, just a temporary shortage of processing in mills.

- Copper demand has been surprisingly strong despite the covid situation, and much of that has to do with a “green” push by governments into EV’s and such – I expect copper to remain strong in the coming decade.

- Uranium just overcame the biggest supply glut ever with the Japanese nuclear shutdowns post Fukishima, and we are set for a large number of reactors coming on line in future years.

- Precious metals are simply a great semi-defensive bet when interest rates are forced super low worldwide, and I expect gold to see steady strength this coming decade as much of the world tries to reduce its heavy reliance on US dollar assets. Crypto may have been a somewhat bearish influence in the past as it pulled speculative money from hyperinflationists and such, but the technology will be long term bullish from gold as countries such as China will use it to expand their international trade into digital Yuan, bypassing the US-dominated Swift payment system and helping them reduce their need for US dollars to facilitate foreign trade.

I’ll stop there. Good luck trading and developing your overall market thesis. Remember that anything can happen, the market is in an extremely volatile position, and now more than ever you need to keep the mental flexibility to ask yourself “what if I’m wrong” no matter what your market view is. This is certainly the most exciting market I’ve traded!