Gold has many drivers and many narratives. While much of the mainstream investing news talks about gold in relation to the federal reserve, or the US CPI, or some kind of warning about US deficits, the truth is that this is just noise. The western financial news is puzzled by gold’s moves because western investors didn’t start this move.

The current rise in gold started with central banks in China and emerging markets, then moved on to people in China finding a new store of value after Chinese Real Estate started turning, then it grew and moved on to citizens of other countries as the US Dollar started out-pacing their currencies.

In fact, western investors have been selling out of gold ever since the peak in August 2020, and they just started buying back in March this year. How can you tell? Foreign investors in places like China, Japan, and India tend to invest in physical gold bars and jewelry rather than ETF’s and minings stocks. In fact, many foreigners are unable to buy listings on the NYSE or NASDAQ just like most US investors are unable to buy stocks on foreign exchanges. Here’s the chart:

As you can see, GLD has been selling off for quite some time, it has only started to get significant inflows in March, and its assets under management are still significantly below those in the April 2022 and August 2020 peaks. As goes GLD, so goes GDX as you can see below:

The gold price climbed as foreign demand has sent it to all-time highs. GDX is much more like GLD – significant inflows didn’t start until March, and the move is still nowhere near the peaks in April 2022 or August 2020. Retail investors haven’t really entered the space yet, so non-producing explorers are still sitting at 5-year lows.

I still think that this move in gold is just getting started. I have this image in my head of enormous streams of money that once flowed into Chinese real estate now diverting towards gold. As Chinese real estate once soared to unimaginably crazy highs, so can gold.

This will not be enough to raise any of my gold mining stocks though, I need western investors for that, and they are just starting to arrive. With the unrelenting rise of gold in the headlines, more and more western investors will be attracted to the space and we’ll see a serious spike in the tiny gold mining sector.

How will I be able to tell when the party’s about over? I am following the basket of non-producing explorers that I once owned. I dumped them a couple of weeks ago to shift into royalties and producing miners with real cash flow from production only. My reasoning is that we have elevated risks of recession and that recessions in the past tended to see gold tank along with the miners, then recover to new highs in a fantastic v-shaped way. I prefer to be in cash-producing companies if this happens. Anyway, once these non-producing explorers start to soar I’ll notice, and then I’ll start reducing my mining stocks.

That’s all for now, good luck riding this crazy gold bull. Here are my latest allocations:

As you can see with the charts above and my notes, I’m trying to find a decent target to reduce but the most I can really do is say that I don’t think they’re done climbing yet. Perhaps we have another $100 in gold before it pulls back, but the gold price is still moving on this wall of investment money, largely from China, that won’t be effected by western metrics. There are worries of a CNY devaluation and the Chinese mainlanders really don’t have many ways to hedge that outside of physical gold, especially during a major housing downturn. The COT report shows that many of the miners are hedging – and non-commercials/speculators are taking the long side – but levels are nowhere near those of March 2022.

I still think that junior miners aren’t moving much because western investors haven’t really bought into this rally yet. They’re starting to, but these spikes can be so fierce that they can run out of steam anywhere from the April 2022 peak above 50 or the 2020 peak at 65. I think GDXJ of 50 – which is 20% higher than here – is probably a good place to reduce risk. Whether that means just selling off my long calls, selling covered calls, or reducing my holdings significantly is undecided.

I had already decided to get rid of my explorers, and last week I did just that – only keeping one PM explorer because it is currently locked from trading due to an acquisition. I also decided to dump SILV because they had disappointing results, reducing estimated mine life, and I decided to re-allocate it into PAAS which still has potential upside surprises in some of their mines. I chased into PAAS just to get a starter position, but that stock has been shooting higher recently and not giving dips to buy. I’m trying to stay patient, as I still have plenty of silver exposure elsewhere.

I also added more BTG (Rick Rule liked that one and it hadn’t sprinted too far yet), and more to a few of my royalty stocks like EMX and UROY. I would like to add nickel exposure with LZM but I feel the trade is too early – perhaps in October I’ll have a good opportunity to enter that and buy more PAAS. Rick Rule is also particularly bullish the Lundines – a successful copper mining family in South America – so I chased a starter stake into LUNMF.

Uranium miners have been hotter than ever these last few weeks. I don’t want to sell anything, but its a tough time to add to the sector.

As for everything else … I’m still anticipating a significant move in US Cannabis once the FDA reschedules it prior to the election so I’m sitting there. TLT is dropping a bit, but it tends to drop after June, bottom late October, and then rally through January. I’ll keep this in mind when my covered calls expire in June. XRP is a 4-year crypto hype-cycle play and I plan to dump it next march into the next crypto spike. DOCN is just a cloud-computing company with crazy expensive calls. An at-the-money covered call expiring in January 2025 is still selling around $8.15 for a $37.32 stock which is a 22% up-front premium just to hold it for 6 months. LTBR is a similar story – its a Uranium fuel company I’m not particularly comfortable with, but the calls are so expensive that I just keep selling them for the premiums.

As for the S&P 500 – it looks like it’s ready for a pullback to me, but I really think anyone who wants to bet bearish would be better served betting against the struggling giants of the space. AAPL & TSLA are in clear downtrends and AMZN is just hitting resistance at its 2021 peak. NVDA looks like a potential blow-off top, but it’s too expensive per share to touch put options on it.

My reasoning for this approach is that the structure of the cap-weighted S&P 500 index funds tends to reinforce momentum, with support from flows weakening on the way down and strengthening on the way up. Money is still piling into S&P 500 index funds, ironically looking for safety through diversification, and the buyers tend to be sit-and-forget retirement account investors. While this structure has dangers, I don’t think we’re near crashing, but it doesn’t matter because any weakness will hit the struggling giants like AAPL, TSLA, and AMZN the hardest anyway so those are just simply better downside bets.

Here’s my latest portfolio. Last week I had significant margin with cash at a -3.7% weighting, but after my ripping-the-band-aid approach to selling my explorers and Silvercrest I’m sitting on positive 6.3% cash. Unless theres a good dip for me in LUNMF or PAAS, I’ll probably stick this in something like VUSB (short-term bond fund) so that I can get dividend payments while I wait.

The reason I picked on LGDTF in particular here is because it is my largest gold explorer holding. It is one of many gold exploration stocks that has a great story. Here’s the description from its website at https://libertygold.ca/

Highly valued but increasingly rare, oxide gold is the signature commodity for building low-cost, heap-leach, open-pittable mines. At Liberty Gold, we are 100% operator of not one, but two oxide gold projects in America’s Great Basin, one of the world’s friendliest mining jurisdictions. We are advancing Black Pine, a large highly prospective mineralized oxide gold system in Idaho whose true value and size is only now being unlocked; and Goldstrike , an oxide gold resource in Utah at the PEA stage. Combined, we are building toward a multi-million ounce oxide gold resource, creating exceptional shareholder value at scale.

Doesn’t it sound fantastic – lots of producable gold in an ultra-safe US jurisdiction? Well, as Rick Rule says, mining exploration companies are like salesmen shouting for someone to look at their potential resource. They raise cash and drill holes to show everyone how valuable it is in hopes that someone will buy it from them and put it into production. The problem is that you can wait for decades and most of these resources still won’t become viable mines. Even worse, these explorers heavily dilute existing shareholders over time as they raise money to drill, promote, and expand their claims.

If you don’t get some kind of buyout or some kind of development towards producing from that claim within a few years, your shares can get so diluted that you’ll never see that initial investment again, even if it is acquired for development a decade later. From that standpoint, retail investors like myself should avoid non-producing explorers entirely unless they have such an amazing claim that its bound to be purchased and produced by someone in the near term – like Snowline Gold or NexGen Energy.

Retail investors like me will still want to participate in a serious mining bull market, but there is another way to invest in new mines without being endlessly diluted. Specifically, Royalty companies.

Royalty companies acquire agreements to receive either a percentage of revenue or a percentage of the minerals produced at a particular mine. Exploration companies are always looking for money to further their claims, and they will often be willing to give up a small percentage of production in order to get that funding. However, unlike with stock shares, these royalty claims can not be diluted over time.

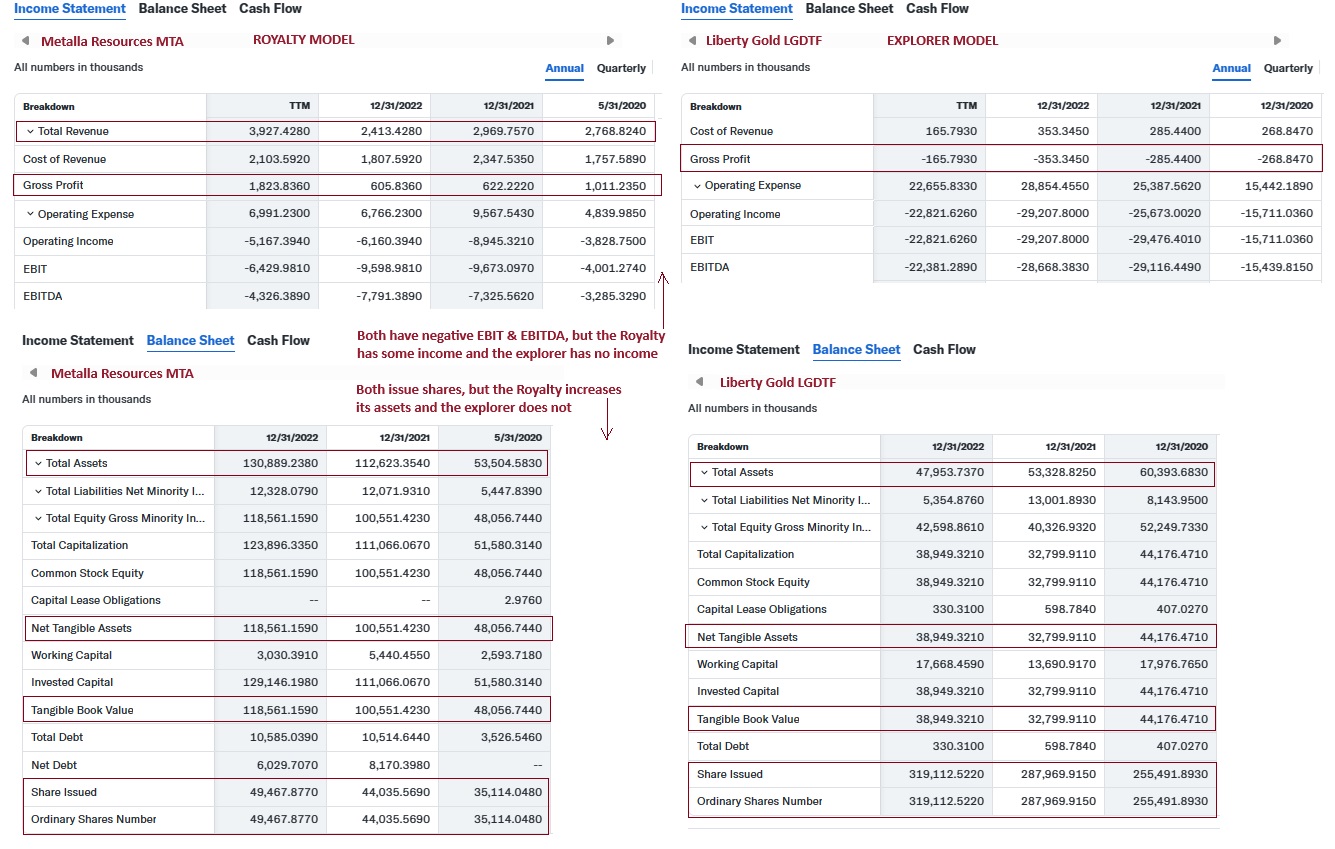

So how are royalty companies performing today? Here is my largest holding, Metalla Resources:

Do you get diluted in royalty companies like Metalla? Unfortunately, the answer is yes – this is true of any company that has negative earnings year after year. On the other hand, look at this key differences in the income and balance sheets (from Yahoo Finance, with the financial statement truncated):

You can see the big difference above … with a royalty company, I can hope for shares to regain prior highs while I honestly can’t with an explorer. With Metalla in particular, a lot of the money they have spent and the shares they have issued have gone toward acquiring new royalties or helping to develop existing ones. Their income comes from (5) royalty streams which are currently producing, it will rise as the (37) royalty streams at mines under development come online, and they have additional growth capacity from the (37) royalty agreements they have with developers.

The reason that Metalla has been such a dog for the past decade has everything to do with the post 2012 oversupply in mines, as production from the great 2000’s bull market all came online and the prices of the metals fell. QE and zero interest rates couldn’t save the mining industry from this vast over-supply, and royalty companies saw projects they had interest in get shelved while active streams declined over time as mining companies had to consolidate and reduce production.

If a serious bull market in mining is underway, and the oversupply situation of the last decade has finally come around to an undersupply situation that will incentivize new mines to come online and old mines to invest in expansion, then royalty companies will stand to benefit greatly – just like they did between 2000 and 2012. I support this view, and I plan on holding royalty companies here, but I also want to get rid of my exploration stocks.

That leaves the question … how do I get rid of these things? Should I just sell them all and take the tax losses over years, or should I wait for some interest to return to the sector?

Ultimately, I have decided to view these exploration stocks as gauges of sentiment in the sector. The fact that these explorers are sitting at 2016 lows means that the sentiment is in the garbage, and I might as well wait until it improves. Gold is clearly breaking out to all-time highs, but this is due to physical buying in places like China and Japan. Western investors prefer ETF’s, and those have been selling off like crazy:

As long as gold continues to make headlines, interest from western investors and institutions will start to return to the sector. This will culminate into a big spike which brings everything in the sector along with it, as often happens with the small and illiquid stocks in this sector. How do I know interest will return? Take a look at my largest holding, which is significantly in the green at this point. The smart money in the mining sector knows guys like Ross Beaty, and this is an early sign of their interest:

EQX is one of my mining stocks which is well into the green. I am trying my best to avoid taking profits until overall sentiment in the sector comes out of the garbage – even though I still sit on expensive margin. I hope to see a jump in my exploration stocks this April so that I can sell some off, but I might just hold a negative cash balance until June when my covered calls on TLT expire and I can sell some of that off.

After the long workweek, I woke up early to spend the day snowboarding yesterday. While it was a lot of fun, I am woefully out of shape from working in front of the computer all day, so I’m just going to write a quick post on my iPad. Here goes…

While many in the world of twitter finance are discussing the hidden strength of today’s economy, I see things as very much divided. Those who were hit hard by the GFC, especially those graduating into it, never recovered. Those who were not effected much by the GFC often don’t know the term, remember it vaguely as a recession in 2008-9, and they don’t acknowledge the massive changes to the economy post 2009.

These massive changes include the passive wave pushing up the biggest stocks relentlessly while crushing value stocks, flooding the labor market with online jobs postings that collect many resumes but have no intention of hiring, crushing housing construction then bringing in wall street and house-to-hotel conversions through AirBnB, creating gig apps allowing anyone to sign up for Uber driving and deliveries with no connection to the demand for such services, and outsourcing much of the US manufacturing base. This was all prior to the 2020 pandemic.

The pandemic response changed things even more rapidly, leading to unprecedented levels of supply destruction, small business destruction, and wasteful government spending. After 2021, approximately 10M undocumented immigrants entered the US and have not been accounted for in the labor force, further skewing the jobs data while creating massive inflation in food, housing, and healthcare (every human eats, sleeps, and goes to the ER when necessary) much of which is paid for in massive local government deficits.

We have never seen a situation like this in the history of our country, and parallels to past events miss many of the modern nuances. It makes a lot of sense to me why some expect a depression-level crash any day now while others expect stocks to continue their assent for many more years.

Most cash flows into markets are totally unrelated to valuations and enter momentum-chasing structures like maket-cap weighted funds. Young people are giving up on family raising in unprecedented numbers in many countries throughout the world as the coat of basic living soars in relation to middle class wages. Those with access to some capital don’t see a way to work their way out and are driven to gambling on the markets much like the famed shoeshine boys of the 1920’s. Does that mean a Great Depression and crash are coming? Its impossible to tell because so many things about society are vastly different today.

If austerity wins the day in politics, a Great Depression can ensue, but it doesn’t seem to be going that way. If ever-more government spending is the result then it can lead to prosperity if it is spent productively like the post-WW2 movements with massive labor strength, wage gains, highway and housing development, consumer goods building, and the massive Marshall Plan spending to rebuild Europe. It can also lead to unprecedented shortages and extremely high inflation if the spending is done poorly – like building massive new infrastructure for the highly resource-intensive wind, solar, and EV development while continuing to divert food into biofuels and flooding the country with people with no plan and no path to living wage incomes.

All of this is happening with the some of the most self-righteous and out of touch leadership we’ve ever seen in all of the major countries. Anything can happen next, especially in capital markets.

This week’s trading:

I added more BTG (junior gold producer with high dividend and a mine finishing up in Canada) and I bought back my covered calls in UROY (Uranium Royalty).

I still see Uranium in a long-term bull market with a pullback that isn’t necessarily over, but the UROY calls went under 5 cents so I might as well re-gain the opportunity to sell them again on a spike.

As for my precious metals miners, I still think we’re early in this move which I see as more near-term. Physical buying, particularly in China, has lead the metal to all-time highs and is just beginning to get the interest of western speculators who have been selling out of the gold and gold mining ETF’s these past 2 years. Gold miners tend to spike and crash, and I’m still deciding on how best to see when sentiment has become too hot. My gut says to watch the a non-producing explorers as a spike in those is a great sign of speculative sentiment entering the space. These haven’t really budged yet.

That’s all for now. I advise everyone to keep an open mind to the direction of financial markets, enjoy life, and don’t get emotionally caught up on things you can’t control.

I’ll start with my thoughts on the S&P 500. I have heard plenty of takes, including many that call for a downturn due to lagged effects from interest rate hikes, bank trouble stemming from commercial real estate, a looming recession, and so on. However, I believe the only way to play the S&P 500 is with momentum. You need to respect that any link between the economic fundamentals and the S&P 500 is broken, and that the economy could be quite weak while the S&P 500 continues to rise.

The wild swings in market cap from the biggest market cap stocks like NVDA – which went from under $250 per share 1 year ago to $878 per share today – should be solid evidence that the money driving these things is not guided by fundamental projections. Simply put, we have had an extremely weak economy for quite some time, shown in weak numbers for things like stagnant or falling full-time employment, reduced number of quits, reduced hours worked, and so on and it hasn’t made the S&P 500 index fall. At the same time, we have two presidents who are known to be big spenders and a number of inflationary forces at work in our economy today. These forces do not include wage growth – which always follows rather than leads inflation.

Inflation stems from high government spending in resource-intensive projects like subsudized wind, solar, electric vehicles, charging stations, and war materiel. In addition, the enormous immigration we have been seeing is highly inflationary. While it is theorized to be deflationary by hammering down wages, the type of non-skilled immigration we are getting is simply leading to a lot more people signing up for gig work apps, competing for a small and amount of available drives and deliveries that really isn’t growing. At the same time, they all require food, housing, and medical treatment which has been leading to an absolute blowout in budgets of major cities throughout the US. Massive spending and resource use for minimal production is inflationary.

Gold has been spiking for a different reason, which I’ve been mentioning quite a bit. The enormous savings of the well-to-do Chinese that previously went into their housing sector is being increasingly diverted to physical gold bars and jewelry. This is because their investement opportunities are very limited – they cannot buy foreign stocks, bonds, or crypto for example. I believe this trend will continue for some time, and this will drive the gold price higher.

The all-time highs in Gold have been starting to generate some media attention in the west, and has been starting to get interest in related sectors the western way – which involves more purchases of silver and mining stocks. Precious metals investments in the west have been such a disappointment after the euphoric expectations of early 2021, that many have given up on the sector entirely, so we are starting a rise from low sentiment in my opinion.

Gold and silver tend to do well in spring – roughly peaking in late March to mid April – and I expect a similar pattern here. My plan is to wait a few more weeks, and if I see the movement I’m anticipating, I will use the opportunity to sell off many of the explorers in my portfolio.

These gold and silver explorers, who own significant claims and drill holes to map it out but have no revenue, have been a disasterous investment. They dilute shareholders over time to get money to drill and you’re left hoping that they get bought out our hyped up before your shares are diluted too much. Royalty companies, such as MTA, EMX, SAND & UROY, and so on have a much better way of getting exploration exposure without diluting you. The reason is that these companies have very low internal expenses, so most outflow is to purchase royalties which gets desperately needed money to explorers. At the same time, the royalties are land rights which are not diluted when the explorers issue more shares.

The royalty companies I hold still depend on those royalty claims eventually turning into mines. MTA for example owns only a few producing royalties, but a lot of royalties on developing mines as well as areas held by exploration companies. If there is serious mine development, they will do very well. If not, we have seen the share price collapse from a 2020 peak of $12.50 to very recent low near $2.30. Despite this, I am happy to have as my second highest mining position. By contrast, I simply don’t expect the bulk of my exploration companies to recover their former peaks.

Mining companies which produce revenue and are building out existing mines are tremendously undervalued in my opinion. These dominate my top-held mining positions like EQX, NEM, AG and SILV. These companies have the generated profits to avoid diluting shareholders while they slowly develop new mines and expand existing ones to improve their profitability over time. I tend to be very lenient about their expenses over the past couple of years because mining shares were so cheap relative to gold and silver that I expected them to be expanding production.

For Uranium miners, I am still happy with my positions and my strategy of riding the bull market while selling significantly out-of-the-money covered calls at sentiment peaks. I aim to re-allocate more to the sector but I am trying to remain patient about it as the sector continues to consolidate.

This week I added shares of UUUU as it fell below $6. I wanted to add something, but it’s too early to buy back into URG without triggering wash sales, I’m reluctant to add to UEC and CCJ so much higher than the covered calls expired at, I’m reluctant to add too much more to non-producing explorers, and UROY is already my biggest position.

Aside from that, I added a new gold miner, ticker BTG, after hearing the CEO speak on Kitco. They are similar to EQX in some ways – a mid-tier producer with significant production investment in properties they already own (and recently acquired in some cases), a potential flagship mine under production in Canada, and a projections of 700-800k annual gold production in the next year. This one also boasts a 6.1% dividend yield. Anyway, I may add more to it because it’s incredibly cheap today just like EQX.

Many of my recent investments have been on margin, hence my negative cash balance. There are times to buy and times to sell, and they don’t tend to coincide. While I realize that paying crazy 13.5% margin rates that are not tax deductible is a losing proposition over time, I have eased up a bit figuring that I could reduce it in a few weeks by selling off some of my PM explorers, and if that doesn’t work I could simply sell off some of my TLT shares once the covered calls expire in June.

Anyway, that’s the current plan. Here are my latest allocations:

I’m going to start with charts today, then discuss my opinions on where things are headed and why.

The S&P 500 is still sitting at all-time highs. This isn’t a trend I want to short right now, but I’m not long this beast either. Most of the money flows are going through passive funds, and that creates a market that is quite illiquid, despite the significant volumes traded. The reason is that only a small portion of this market actually reacts to price … large, regular flows come in from buybacks and 401k flows into index-tracking funds as momentum traders join in and more insiders sell shares at all-time highs. While a reversal in passive flows can easily create a vertical crash like we saw in March 2020, I don’t expect these flows to reverse in the near term. I anticipate significant rotations within the S&P 500 and I believe there are better opportunities trading those. For example, some of the biggest stocks such as Tesla, Apple, and Google have come down significantly off their highs – and with the index rising, other names must be gaining quite a bit.

This chart of NVidia, now the #3 company by market cap which individually makes up 4.6% of the S&P 500 valuation, shows how illiquid these moves are. The past 7 trading days saw 5 significant gaps higher at opening, as the stock rose from $780 to a peak of $973 on Friday morning (up nearly 25%) and then fell nearly 10% to end the day at $875. Articles abound on how much market cap value NVDA “lost” in that 10% drop, but they fail to mention that these valuations are all a mirage to begin with because a fraction of a percent of the company’s $2.2 Trillion market cap will cause wild swings in the share price.

Anyway, I don’t plan on trading these at the moment as my current focus is on gold.

Gold has clearly broken to all-time highs.

The large gold miners have broken off their recent low to the upper range of 2019 valuations – when gold was consolidating at $1500/oz, about 2/3 of todays’ price.

Junior gold miners have broken off their recent lows to the bottom range of the mid-2019 consolidation.

Here’s what I believe is happening. Central banks around the world, especially in China, have been buying gold as a way to diversify their holdings away from Western currencies which could be affected by sanctions in the event of a conflict. Perhaps a bigger force is actually buying pressure from the well-to-do in China itself. Most people don’t realize it, but people in mainland China are not allowed to buy foreign assets like stocks and bonds. They can invest in Chinese stocks, Chinese bonds or bank funds, Chinese Real Estate, and physical gold like bars and jewelry. As Chinese real estate deflates, the large builders go bankrupt, the stock market is hovering near 2-year lows, and stories of scams in the banking sector are rampant, gold purchases in China have been absolutely soaring.

Imagine all the money that it took to build up the biggest housing bubble in the world – and then imagine a portion of those cash flows turning to physical gold. This has driven gold prices to all-time highs despite the rapid selling of gold from ETF funds.

I see a perfect storm for gold miners. Physical gold buying is not done for short-term trades because the transaction costs are too high, and there is no sign that the buying of gold in China will abate soon. The COT reports have also shown commercial short positions reducing into a rising gold price, which is unusual and bullish.

As physical gold breaks to new highs, momentum investors will inevitably chase it higher and start putting money into the gold miners. Billionaires like Stanley Druckenmiller are already putting money to work in the gold mining space. I believe that these miners are getting ready to jump significantly over the next month leading to retail FOMO jumping in, which will create a spike in the share prices. These spikes do not tend to last, and I will be looking for signs of things peaking with thoughts of the Silversqueeze peak and what that looked like.

As you can see above, Barrick Gold traded just like a levered version of the gold price. This was probably partly because ETF’s were newer and smaller … GLD didn’t exist until the end of 2004, GDX came out mid 2006, and GDXJ came out in late 2009. In the 2000’s, value stocks were king and tech stocks went nowhere.

The above chart looks tempting to follow, but some things just don’t seem to fit, like why does the “First Sell Off” to bear trap last for 4 whole years? We’re in a fast-moving meme stonk world today, and I expect news coverage of gold hitting all-time highs to bring in a wave of short-term FOMO that creates a peak and a crash similar to the March 2020 to March 2021 period, only this time I intend to jump ship when sentiment peaks.

What next? Uranium. Uranium miners are in a real long-term bull market and I fully intent to reallocate there as the spike builds up.

You can see the recent pullback, which is quite significant, but I still think we consolidate a bit further, perhaps pulling back to the 200 day moving average which is another 10% drop or perhaps doing nothing for a number of months. Regardless, I favor gold miners in the short term, but I believe that the Uranium bull market will last longer and move further than the gold bull market does.

Silver is a much more difficult market to gauge, but I the silver miners tend to trade in lock step with the junior gold miners (SIL and SILJ look a lot like GDXJ) so I intend to trade them similarly. Silver does have large industrial uses, especially with wind, solar, and EV’s, but some things have me worried about demand keeping up in those sectors. Even as governments continue to plow wasteful spending into these technologies, the enthusiasm for them are waning. Take a quick look at these pictures of the Chinese EV graveyards: https://www.bloomberg.com/features/2023-china-ev-graveyards/

For now, EV production is set to continue as governments like my home state of California push requirements to electrify everything and build out massive new EV charging infrastructure. This will be great for the mining sector in general while it lasts, but I believe it will peak out in a Fukushima type bang. We’ve already likely seen peak EV production as hundreds of Chinese EV companies that were fake-selling EV’s to fake ridesharing companies to get government and shareholder money are going bankrupt and shutting down their facilities. The next wave of EV building will have much less government support and will require a lot more buyers to show up, and they clearly aren’t. Our major dealerships are crammed full of large, expensive EV trucks that no one is willing or able to buy as they curtail production and turn back to hybrids and conventional ICE vehicles.

The next phase seems as inevitable as it is terrifying – the Chernobyl moment for EV’s. Most people don’t realize that lithium-ion batteries are extremely unstable and flammable. They burn much hotter than gasoline fires, reaching 5000 F (2760 C), making fires spread very rapidly from one to another. To make matters worse, these fires are both highly toxic and very difficult to put out as the batteries contain all the oxygen needed to keep those fires going.

Take another look at the pictures of EV graveyards in China. How long until just one of those batteries degrades or breaks in the wrong way causing it to go up in flames. You can quickly have an enormous fire spreading toxic metals in a wide cloud over a large area. However, unlike the radioactive cloud from Chernobyl, the danger from these toxic metals doesn’t dissipate over time – it has to be cleaned up and that process is painstakingly difficult and expensive. Chernobyls, cloud didn’t cause all of Ukraine and eastern Europe to abandon their homes, but clouds from massive EV fires could pose that danger in China. If that happens, expect sentiment for the EV movement to shift rapidly, leading to solutions that are much less metals-intensive and leaving the mining industry once again in a period of significant oversupply.

I hate to leave things on such a somber note of environmental calamity, and I do intend to focus primarily on things we can control, like where to place bets on the markets, rather than things we can’t like politics. So I’ll just say that my long-term expectations for the mining sector in general are somewhat tempered and leave it at that.

Last week I added significantly to SBSW as it was beaten down to a pulp, and I still see more near-term opportunities in gold and silver miners than I do with Uranium. I am trying to be refrain from buying too much though, because my cash balance is already negative and my margin interest rate is a non-deductible 13.6% – so using it for anything other than taking advantage of a very temporary buying opportunity is a losing proposition.

As you can see, gold looks like its ready to push out to new highs while gold miners are still carving out a bottom. My preferred narrative for why is that the big buyers right now are foreign central banks and individuals guarding against local currency depreciation.

The Chinese have been particularly big buyers of gold. Individuals living in mainland China tend to have limited options in where to store their wealth. With the real estate bust in full force along with defaulting loans from developers and other companies, they are getting wary of parking too much into real estate. Bond funds don’t pay that well either, and some are nervous that the principal might not be safe. Chinese stocks have been hit especially hard these past few years. That leaves gold, and they are buying a lot of it.

Meanwhile, western investors are still looking to the S&P 500 as it continually shoots higher, the new spot Bitcoin ETF’s are starting to get significant inflows, gold in US dollars looks like its been in the same boring range since August of 2020, and gold miners aren’t getting any positive momentum.

I have a hard time imagining a serious breakout in gold prices that leaves all of the miners behind. In addition, I’m more excited than ever about the ability of producing miners with good cash flow to lock in some significant new gold mines at relatively low costs and extend their cash flow out for decades. Newmont, NEM, is one of those companies, and it has recently purchased Newcrest, picked its top assets, and put some of its assets up for sale to build up funds for a new flagship mine purchase. They also recently cut their dividend in order to save up for this, with speculation that they are looking at explorers with big finds such as Snowline Gold (SNWGF).

I just imagine the near-zero earnings of the past year plowing into their flagship mine buildout in Canada and their significant mine expansions in California, Brazil, and Mexico. Then I imagine what those earnings looks like when their Canadian mine comes online (estimate is the first half of 2024), their gold production nearly doubles, and their expenses from the mine buildout disappear.

Simply put, if their revenue nearly doubles as their earnings soar, I can’t imagine this stock going anywhere but up. As a result, I continued to buy the dip and added to my shares significantly this week. At the same time, I sold off the Uranium miner I added last week, URG, and I sold off the Sprott physical platinum/palladium trust SPPP in order to reduce my margin.

Quick note on my US Cannabis companies – I’ve been seeing posts from @todd_harrison on Twitter about many of these companies re-filing their tax returns from prior years and getting refunds. Previously, as sellers of an extremely dangerous schedule 1 restricted drug, all standard business deductions were ineligible and all gross profits were taxable. The re-scheduling of Cannabis to schedule 3 hasn’t been officially announced yet, but it will change the illegal industry status and allow standard business deductions. Thoughts are that the official announcement will come a month or so before election day to motivate voters. Meanwhile, if these companies are re-filing tax returns from prior years and getting big refund checks, it adds a bunch of cash to their balance sheets while making chances of a positive rescheduling announcement more likely. I’m certainly bullish on this sector, but for now I’m just planning on sitting on my shares rather than adding.

I’ll start with a chart of the S&P 500. I’m not long, but I’m not comfortable shorting this either.

Now on to gold miners. Seasonally, late February tends to be a low point for the sector.

Gold miners certainly look to be carving out some lows. I’ll start with the 5 year chart of GDX, where you can see the price is still at levels breached in 2019.

Next I’ll show the 1-year chart of the mid-tier and junior miners, GDXJ, which just tested its October 2023 lows. If you look at its 5-year chart, GDXJ is actually lower today than it was 5 years ago even though the price of gold went from $1300 to $2040.

Some of the reasoning I’ve heard behind the price of gold vs the gold mining stocks is that emerging market central banks have been buying up physical gold to diversify away from foreign currency risk and counterparty risk as well as the risk of being hit by weaponized sanctions. Meanwhile, money and gold tends to flow out of gold ETFs as western investors are cold on the sector. Gold mining stocks have been out of favor for institutional investors for over a decade, and central banks certainly don’t buy them, so these stocks are struggling.

The largest gold miner, Newmont (NEM), just cut its dividend. While this might lose them some dividend investors, Newmont is focusing on taking advantage of today’s low prices to expand production. They recently acquired Newcrest back on November 6th, and they are selling off some of Newcrest’s assets to build up cash for another big purchase so that they can acquire another flagship mine with decades of low-cost production left in it.

Anyway, I have been accumulating gold mining stocks lately, and against my better judgement, I actually purchased more EQX and MTA on margin this week to take advantage of the recent price drops. With margin rates around 13% and not tax-deductible I’ll need to pay this down with my next couple paychecks.

On to Uranium:

I added the junior Uranium miner URG to my portfolio this week because I didn’t want my allocation to the sector to fall too low. Looking at the chart for uranium miners (URNM) above, I probably should have waited for it to turn. Right now, the Uranium mining ETF’s are in a downward channel with the next significant support around 15% lower at the 200 DMA. When these things sell off, they have to sell off their uranium miners and it pushes down the whole sector. If I wait until this bottoms out and turns higher, then I’ll have the tailwind of ETF buying to aid my junior miners instead of the clear headwind of ETF selling ahead.

The one positive sector I have this week is US Cannabis.

My main strategy here is basically to sit and wait. These stocks can’t get any real movement until after Cannabis is officially re-scheduled as schedule 3, which should be a couple months ahead of the election. I’ve been burned enough by the failed congressional safe-banking bills to want to avoid throwing more money at the sector, and I don’t really want to exit until we get waves of acquisitions by big companies like Marlboro and institutional investors picking up shares. Still, its good to see some life in the share price.

That’s all for now, here are my latest allocations:

Last week I wrote about my favorite gold miner, EQX, so I was originally planning on writing about the laggard royalty plays – MTA and UROY. This information is easier to find than normal because there are endless youtube presentations coming out this year’s VRIC conference, so you can get presentations from many of the major mining and exploration companies right now.

This led me to conclude that the problem with MTA and UROY today is essentially the same – they have both been heavily investing in royalties with exploration companies and near-producing miners, and very few of these royalty streams are currently paying. If the price of the underlying metals remains strong, then these mines will continue to build out and the revenue streams will grow. Until then, both of these companies will face heavy losses as their investments outpace their revenues, and they will be reliant on borrowing and selling shares to continue operations.

In contrast, my favorite miners are EQX and AG, which I expect to see considerable growth in revenue and earnings this year. I explained EQX in detail last week. AG is a bit different in that they had one-time costs from their halting of production at Jerrit Canyon and water trouble at one of their silver mines, they are working on getting some revenue out of their ore-processing equipment from mines near Jerrit Canyon by processing other company’s ore, and they just finished creating their own mint for silver bars which will allow them to sell their silver at a higher price point. Stronger earnings should attract more investors while reducing the danger of dilution; instead of selling shares to raise capital, they’ll have excess capital for investing or rewarding shareholders.

As I described last week, the fundamentals behind EQX seemed absolutely incredible while the company traded barely above its Dec 2018 IPO price. As gold has consolidated at, near, and occasionally above its all-time highs over the last 4 years, GDX is down 40% and GDXJ is down over 50% from their 2020 highs. Meanwhile, the charts were starting to look like they have finally carved out bottoms and may be getting ready to turn, just as the gold price brushed to new highs again.

There are many theories about how to trade miners, with narratives of how the senior miners break out first and the juniors follow, or whether the price of gold will go down to follow the miners or the miners will go up to follow gold, so I figured I’d better do a study on how GDX and GDXJ move along with the gold price. GDX started in 2006 and GDXJ in 2009, so I’ll be starting around there.

2006-2010: GDX roughly tracks the gold price until 2008, when it starts breaks much lower as the stock market falters.

2008-2012: Buying price means everything. If you held GDX from the 2008 peak, you would under-perform the gold price for years. If you held GDX from the 2009 trough, you would outperform the gold price considerably to the next peak in 2011.

2010-2014: Both GDX and GDXJ traded together, making a double-top and beginning to fall first 10 months, then 5 months before the gold price peaked. Much like today, the miners fell precipitously while gold prices consolidated horizontally into 2012.

2014-2018: Gold prices carved out a bottom over 4 years of roughly flat prices. Meanwhile, GDX and GDXJ move together forming significant peaks and troughs in between.

2016-2020: GDX and GDXJ carve out two year bottoms between 2017-2019, finally moving back up when gold prices start to climb in 2019. Despite gold prices ending the period with a 16.3% gain though, GDX was down 7.5% and GDXJ down 18.2% over the period.

2018-2022: GDX and GDXJ gain nearly 35 in mid 2019 gold price move. Both gold prices and gold miners reach new highs before the March 2020 correction. While the fall in gold prices is quite muted, GDX dips 40% and GDXJ cuts in half during the selloff. Then both soar to their latest all-time highs in August 2020, coincident with the first gold peak.

2020-2024: As gold prices consolidate horizontally, testing and occasionally breaking all-time highs 4 times, gold miners fall precipitously. GDX and GDXJ form new peaks coincident with each other and with the gold price, but the first two peaks fail to reach the old high and the following peaks were considerably lower. Now we see gold prices above $2000/oz while GDX and GDXJ are bottoming again, lower than the October and March 2023 lows, but still much higher than the October 2022 lows.

CONCLUSIONS:

GDX and GDXJ move together, with the moves in GDXJ more pronounced, especially to the downside. Basically, GDXJ behaves like a leveraged GDX fund.

Note that GDX and GDXJ hold very different companies, but GDXJ doesn’t represent explorers. The top names in GDXJ all have revenues, so they are smaller producers, whereas explorers often have staked claims with no revenue.

Gold miners are instruments to be traded, not owned. They tend to form major peaks and then underperform for years. Even when these peaks are eclipsed, like GDX in 2011 peaking considerably higher than in 2008, the drops in between are brutal and you need a strategy to avoid them.

If you manage to buy near a low, gold miners can be rainmakers. From the 2008 low the 2011 high, GDX soared 250%. From the March 2020 low to the Aug 2020 high, GDX soared 240%. Even when gold prices are flat you can get these moves, like Jan 2016 to Aug 2016 where GDX soared 240%. None of these gains last, they are only there if you take them.

This actually has me thinking that I should be watching GDX and being much more aggressive about exiting the sector entirely rather than selling covered calls on the peaks. Before you get carried away from that conclusion, remember that the last big multi-year bull market in miners was 2000-2008, before GDX was created, and this is how Barrick Gold behaved during that time:

If you’re riding a serious bull market like that one, covered calls at the peaks might be the best strategy. Just never forget the right side, where the gains of the entire period can be wiped out in months.

I’ll leave it there, just know that I’m still feeling very bullish on the miners right now. This week I added a bit more AG and SBSW. Here’s where my allocations ended up:

This week I decided to place a sizable bet on Equinox Gold, so I’ll start by explaining why.

The founder of EQX, Ross Beaty, has been in the mining business for a long time. His last major success was creating Silver Wheaton, which later became Wheaton Precious Metals (WPM). Here’s how he explains Equinox at the resource conference in Vancouver (VRIC): https://youtu.be/FFz5x2U42zE?si=nnNNEW8lCZeYgZG2

Ross Beaty explains how he saw a bright future coming for gold, so he founded Equinox in 2018, with gold sitting at less than $1,200/oz. His goal was to create a large gold miner based in the Americas by acquiring producing and nearly producing gold mines and building them out or expanding them, with a target production of one million ounces per year. The idea is that large cap gold miners tend to get much higher valuations than junior or mid-tier gold miners, and this production number crosses that threshold.

Right now, Equinox has 2 operating mines in California, one in Mexico, and four in Brazil with 564,500 ounces of gold produced in 2023. They are finishing up a new mine in Canada which should be producing in a few months, and they are expanding 3 more mines. All of these projects should complete within a few years which will double their production. The bulk of this increase will be from the new Canadian mine which will hit this year. More details can be found here if you are interested: https://www.equinoxgold.com/

Here’s what got me interested in this particular story, starting with the bullish gold price:

Zooming in, I honestly don’t get much more except that the 50 week moving average is above the 200 week moving average with considerably positive slopes, and the 50 day is over the 200 day with flattening slopes. Messy charts, long consolidations, but bullish.

Now compare this to the large gold miners (GDX) and junior gold miners (GDXJ):

The biggest problem with junior gold miners, particularly the explorers, is that they always need to raise cash. They could be sitting on world-class deposits, but as long as they aren’t producing they can only raise funds to drill, map out the find, and advertise to try to get someone to buy it and build it. If you buy early, you end up so diluted by rounds of share sales that you can never make your money back. However, producers can grow with cash flow and avoid this problem. This is what has been going on with Equinox:

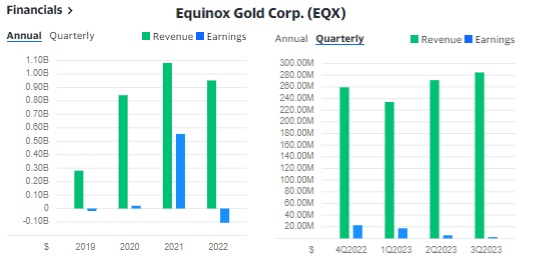

As you can see, Ross Beaty started this out in 2018 by purchasing producing mines, so Equinox was growing revenue. However, revenue stagnated as earnings collapsed after 2021. Why? Because Equinox was using its earnings to fund its mine expansions as well as the completion of its soon-to-be flagship mine in Canada. Building out a new mine costs a lot of money! Ross Beaty expects their new mine to be producing in the first half of 2024, with a targeted production of 400,000 oz at an incredibly low $850/oz production cost. When this new mine is producing, it will nearly double their revenue while the heavy expenses of building out the mine are replaced by the much lower costs of production.

Can you imagine owning a company and watching its revenues double while earnings soar after one short year? Yeah, I’m insanely bullish this one. Here’s the stock chart.

I’ll end it here, as I went long on this one already. As you can see below, EQX is now my largest holding as I liquidated VUSB and added some cash to build it up. Also, I decided to get a little bit of cheap leverage by purchasing $2.50 strike Jan 2026 calls instead of shares. This nearly doubles the number of shares I’m controlling, but it will go to zero if the value of EQX is cut in half in two years’ time. Its a slight risk in my opinion, seeing as how EQX spiked above my break-even closing price in nearly every month of 2023, and for considerable gain if I’m right.